Why Save for College?

Whether you want to save for college for your own educational journey or invest in the future of a loved one, a 529 plan provides the flexibility and growth you need to reach your goals.

State of College Savings

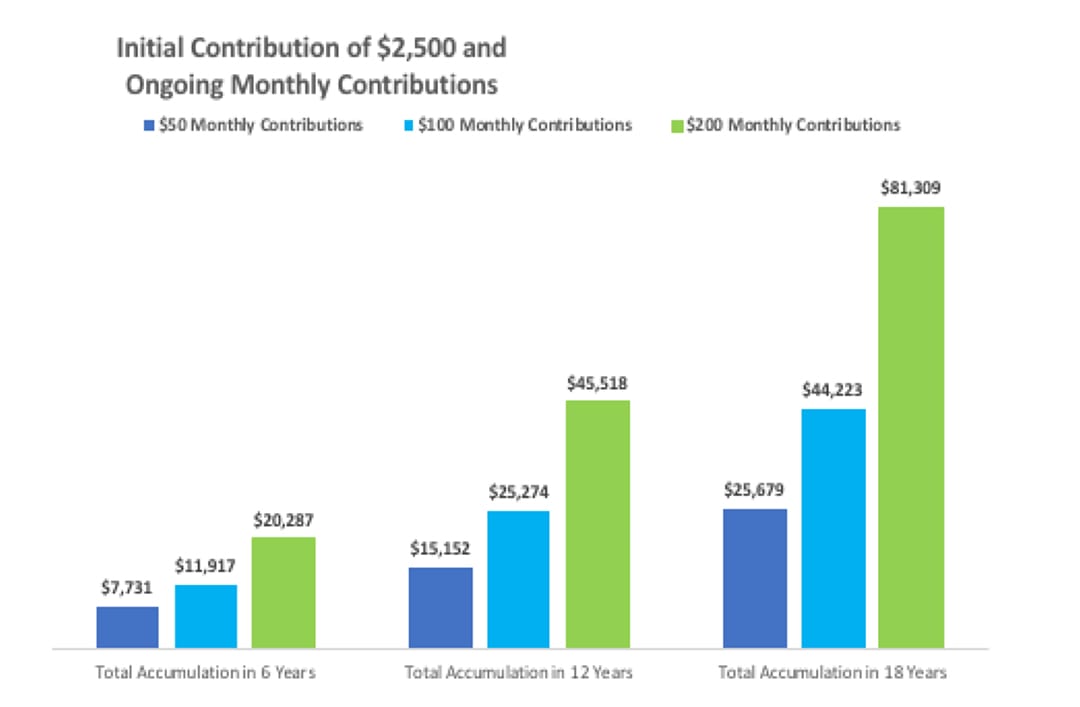

Saving is a critical piece of a family’s overall college funding strategy. The College Savings Foundation’s annual State of College Savings Survey of hundreds of parents showed that those parents who invested in 529s and those who saved with automatic savings plans – each saved more than parents without those strategies. Start as early as possible with systematic contributions – and put time on your side.

This hypothetical example estimates future savings amounts at different regular monthly contribution levels for different time periods. It assumes an initial investment of $2,500, annual investment return of 6% and includes some simplifying assumptions. The information is for illustrative purposes only and assumes no withdrawals during the applicable time period. The illustration is provided by Invite Education and does not represent any particular investment, nor does it account for inflation, expenses, or taxes. Account values will fluctuate with market conditions and other factors, and investments may lose value.

Why Save for College?

Saving for college is one of the most important steps you can take to support you and your child’s future. As the costs of higher education continue to rise, early and consistent savings can help reduce student loan burdens and empower students to focus on their educational choices. A college or technical school education helps build the necessary skills and credentials to achieve higher earnings and career opportunities. Saving early can make a lasting impact on that potential.

What is College Going to Cost?

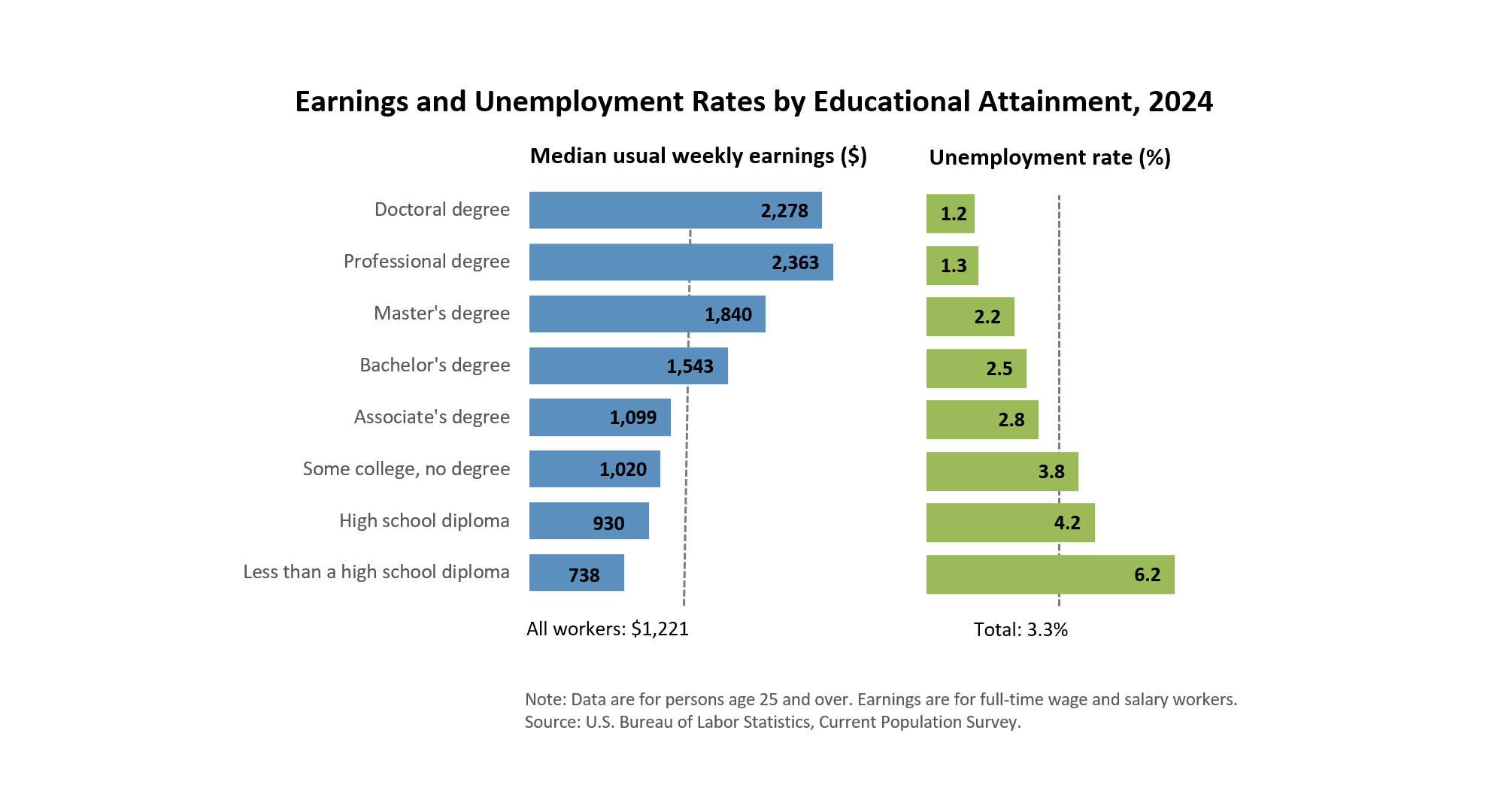

Your goals matter – and a college education can help you reach them. Over time, the income gap between those with a high school diploma and those with an associate’s or bachelor’s degree continues to grow. Research consistently shows that earning a college degree leads to greater financial stability and long-term success. As the cost of living rises, investing in your education is more likely to provide lasting support for you and your family.

Is a College Education Worth It?

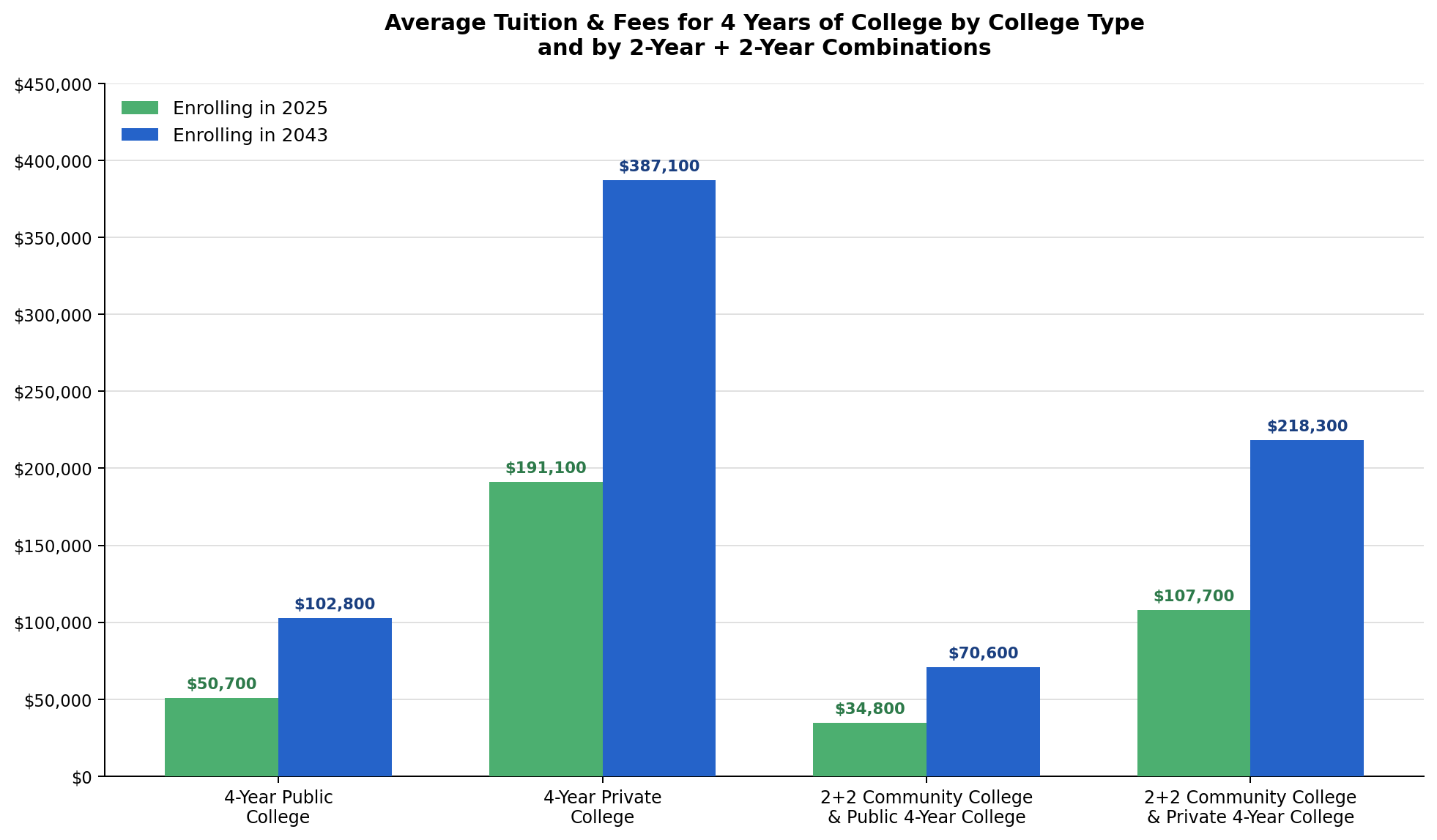

While exact numbers are unpredictable, there’s no question – college can be expensive. In recent decades, tuition has outpaced the overall rate of inflation. But the good news is, there are smart ways to manage that cost. Scholarships, earning college credits in high school, starting at a community college, and planning ahead are all effective strategies.

Projections provided by Invite Education based on average tuition & fees for 2025-2026 as reported by The College Board® and assumed to increase 4% annually. Numbers have been rounded to the nearest $100. (This is a hypothetical example for illustrative purposes only).

How Families Typically Pay for College

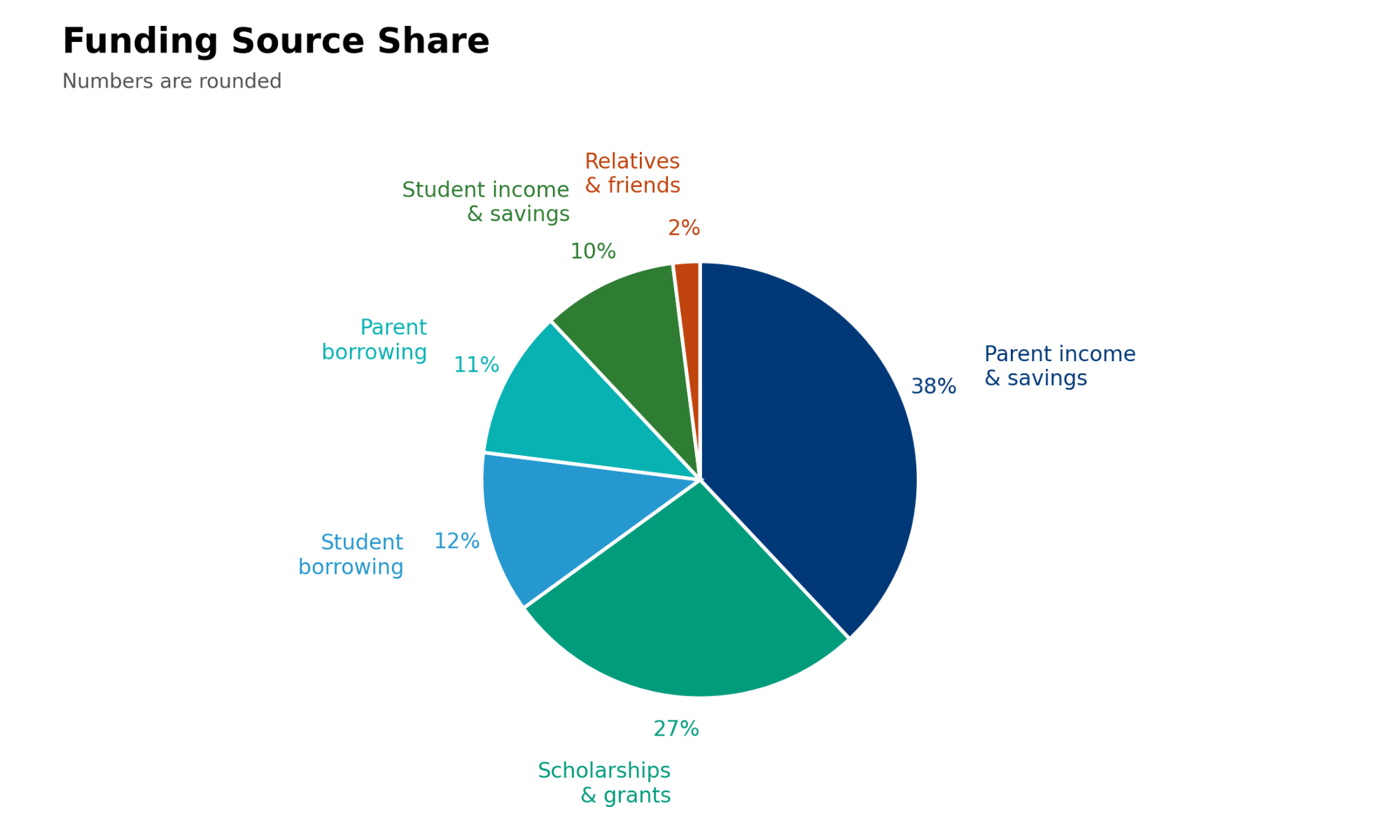

Most families use a combination of savings, scholarship/grants and borrowing to pay for college. In 2024-25, the combined category of parent income and savings was the #1 source of college funding. Nearly half (48%) of college costs were paid out of pocket by a combination of parents’ and student’s income and savings.

Source: 2025 How America Pays for College, Sallie Mae’s national study of college students and parents conducted by Ipsos.

The Benefits of Saving

Student loans are a common way to help pay for college, but borrowing comes with long-term consequences. Student debts can follow individuals for decades, affecting their ability to buy a home, start a business, or meet everyday financial needs. Student loan debt in the U.S. has surpassed $1.8 trillion – more than both credit card and auto loan debt levels.

The rising debt burden can discourage students from pursuing higher education altogether. However, it’s important to remember that a college degree often pays off over a lifetime, leading to increased earning potential and greater financial stability.

The key is preparation. By starting early and saving regularly – especially through options like 529 plans – you can reduce or even eliminate the need to borrow. Simply put: It’s more affordable to save now than it is to borrow later.